Can You Get a Mortgage in Cabo? Financing Options for Foreign Buyers in 2026

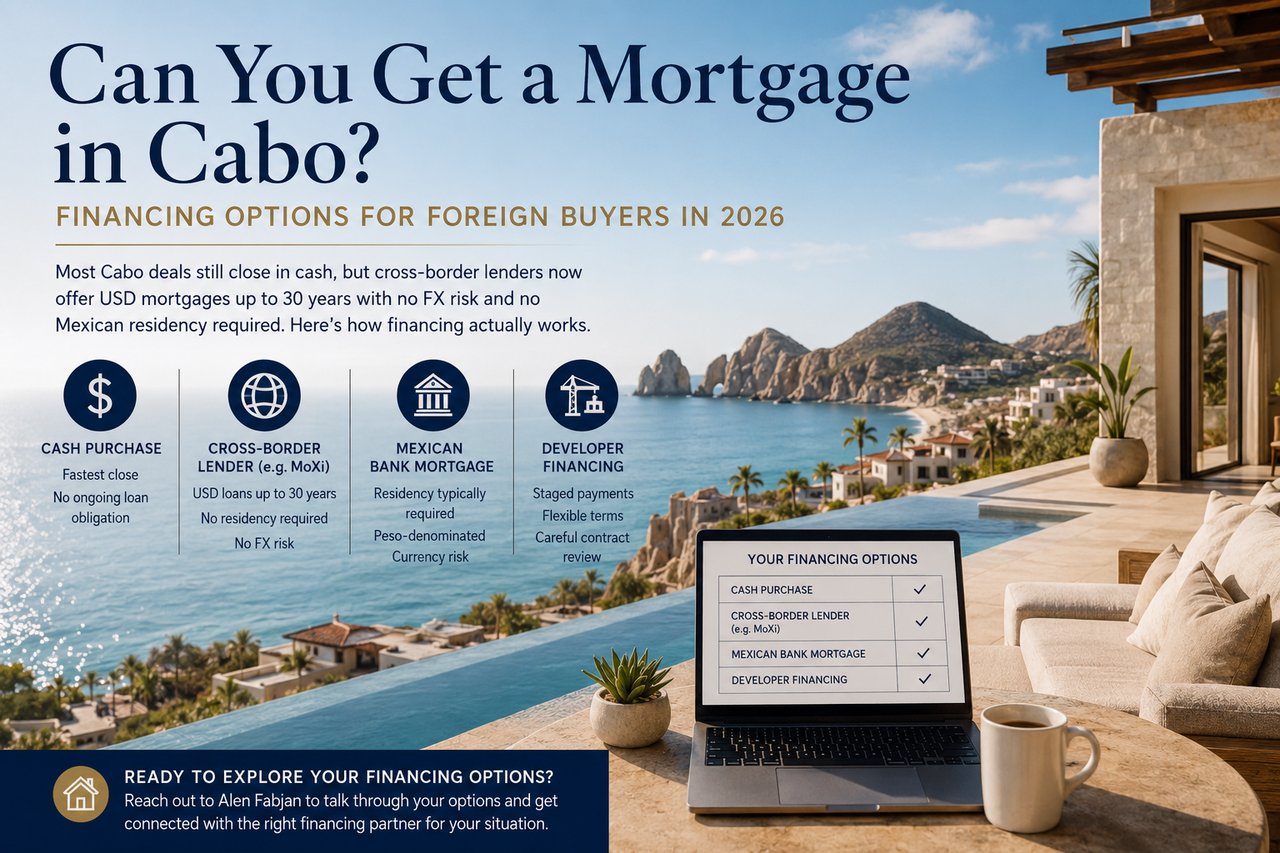

Most Cabo deals still close in cash, but cross-border lenders now offer USD mortgages up to 30 years with no FX risk and no Mexican residency required. Here's how financing actually works.

Ask ten agents in Los Cabos how buyers pay for their homes and nine will tell you the same thing: cash. It's true — the overwhelming majority of luxury transactions here close without a mortgage. But "most buyers pay cash" is not the same as "you have to pay cash," and that distinction gets lost constantly, even with clients who could benefit from financing and never ask because they assume the option doesn't exist.

It does. If you're a US or Canadian buyer looking at property in Los Cabos, you have real financing paths available, and understanding them before you fall in love with a listing puts you in a much stronger negotiating position.

Why Cash Dominates the Cabo Market

Mexican banks have historically made borrowing difficult for foreigners. Without permanent residency, most domestic banks won't lend to you at all, and the ones that do typically demand down payments in the 30 to 40 percent range with interest rates that can run into the double digits. For a buyer used to a 20 percent down conventional loan back home, that math doesn't pencil, so cash becomes the default — not because it's required, but because it's historically been the path of least resistance.

That's shifted. A newer category of cross-border lender now underwrites loans against your US or Canadian financial profile instead of forcing you through the Mexican banking system, and that changes what's realistic for a lot of buyers.

Your Financing Options as a Foreign Buyer

Cross-border lenders. Companies built specifically for this market, such as MoXi (Global Mortgage), lend directly to US citizens purchasing in Mexico. Loans are originated and serviced in US dollars, amortized over terms up to 30 years, and underwritten using your home-country income and credit — not a Mexican credit history you probably don't have. This is usually the most straightforward route for a US buyer who wants a conventional-feeling mortgage experience without the friction of a domestic Mexican bank.

Mexican bank mortgages. Major banks including BBVA, Banorte, and Scotiabank do lend to foreigners, but almost exclusively to those holding temporary or permanent residency. These loans are typically denominated in pesos, which introduces currency risk if your income is in dollars, and they come with the stricter down payment and documentation requirements Mexican underwriting is known for.

Developer financing. On new construction and pre-sale projects, the developer effectively acts as the bank. You agree to a staged payment plan tied to construction milestones rather than going through a formal lender. It's often faster to arrange and more forgiving on credit and paperwork, but the interest rates and terms deserve close review — always have an independent attorney look at the agreement before you sign, particularly around any balloon payment at the end of the term.

What You'll Actually Need

Regardless of which route you take, a few things stay constant. Any coastal property in Mexico — which includes all of Los Cabos, since it falls within the constitutionally defined restricted zone — requires a fideicomiso, a bank trust that holds legal title on your behalf while you retain full rights to use, rent, sell, or will the property. This applies whether you finance or pay cash, and whether or not you hold dual citizenship.

On the numbers, expect a meaningfully larger down payment than you're used to at home. Cross-border and Mexican bank lenders alike commonly ask for 30 percent or more, occasionally higher depending on the lender, the property, and your documentation. Interest rates vary by lender and loan structure, but as a general range, cross-border USD loans for qualified buyers tend to run lower than peso-denominated Mexican bank loans, which is one reason they've become the more popular route for US buyers.

The Real Cost of Cash to Close

Your down payment isn't the whole number. On top of the down payment, buyers should plan for an additional 5 to 7 percent of the purchase price for closing costs, including notario fees, fideicomiso setup, and related transaction expenses. This often surprises first-time foreign buyers who budget only for the down payment before getting the keys.

Financing Options at a Glance

Cash purchase — no down payment threshold beyond the price itself, no interest rate, no residency requirement, fastest close, no ongoing loan obligation.

Cross-border lender (e.g. MoXi) — down payment typically 35 percent , USD-denominated rate, no Mexican residency required, terms up to 30 years, no FX risk.

Mexican bank mortgage — down payment typically 20 to 40 percent, peso-denominated rate, generally requires temporary or permanent residency, currency risk if your income is in dollars.

Developer financing — down payment and terms vary by project, staged payments tied to construction milestones, faster and more flexible underwriting, requires careful contract review.

Frequently Asked Questions

Can foreigners get a mortgage in Mexico? Yes. Foreign buyers, including those without Mexican residency, can secure financing through cross-border lenders that underwrite against home-country income and credit, in addition to developer financing on new construction.

Do I need residency to finance a home in Cabo? Not necessarily. Cross-border lenders generally don't require Mexican residency. Domestic Mexican bank mortgages, on the other hand, typically do require temporary or permanent residency status.

What's the minimum down payment for a US buyer in Mexico? It varies by lender, but 30 percent or more is a reasonable expectation across most financing routes, whether through a cross-border lender or a Mexican bank.

Do I still need a fideicomiso if I finance instead of paying cash? Yes. Any coastal property purchase in Mexico requires a fideicomiso regardless of how it's financed, including for dual citizens.

Thinking Through Your Options

Financing in Los Cabos isn't as complicated as it used to be, but it isn't identical to buying at home either, and the wrong assumption early on can cost you time on a property you're not actually positioned to close on. If you want to understand what you'd realistically qualify for before you start touring properties, that's a conversation worth having early, not after you've found the house.

Reach out to Alen Fabjan managing broker for the Oppenheim Group Cabo to talk through your options and get connected with the right financing partner for your situation.

+1.480.264.1006